.svg)

The core business of Swiss private banks is stagnating - where do the individual institutions stand in terms of profitability, growth and value creation?

In the IFBC Sector Report - Swiss Private Banking, we provide you with our latest assessments of the financial performance and value creation of Swiss private banks. In addition, current challenges and trends in the sector are analyzed. The published annual reports of 31 Swiss private banks provide a comprehensive data basis.

.svg)

.svg)

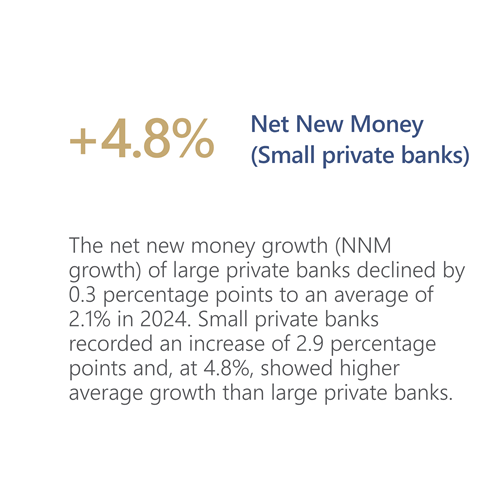

Despite NNM growth and an increasing Return on Assets, small private banks were only able to slightly increase their income from commission and service business on average compared to the previous year, while large private banks had to accept an average decline in their core business. In this context, it is clear that the Swiss private banks will have to ensure a return on the investments they have made in additional client advisors in the coming years in order to maintain or increase their profitability in the long term (NNM growth at appropriate margins).

The takeover of Credit Suisse has shaken confidence in the Swiss banking sector, giving Swiss private banks the opportunity to position themselves as an attractive alternative to the new big bank. In view of UBS's market power, however, this must be seen not just as an opportunity but as a must: If the Swiss private banks do not succeed in positioning themselves in a targeted manner vis-à-vis UBS, there is a risk of additional margin pressure and a decline in core business due to UBS's economies of scale.

The results of Swiss private banks in 2023 were positively influenced by an exceptionally successful interest business. This led to a strong improvement in the cost/income ratio, particularly for small institutions. This extraordinary result must not overshadow the fact that the core business is stagnating or even declining. Profitable growth in the core business should therefore be the focus of strategic considerations in order to maintain or increase profitability at the overall bank level in the long term.

Due to the increasing demands in the areas of digitalization (in particular, customer expectations regarding digital services and cyber security) and regulation, it is to be expected that the cost pressure on Swiss private banks will continue to intensify. In addition, the hiring of new client advisors has led to a significant increase in personnel expenses. Accordingly, cost efficiency must be given greater consideration in order to ensure the long-term profitability of the bank as a whole.

For detailed insights from the study and benchmarks, contact: Christian Hirzel and Noel Sager.

(The document is available in German only.)

More information about our offering for Financial Services.

Also of interest to you, our article on Value-based Management.