.svg)

The significant rise in the market valuations of Swiss retail banks is not supported by an improvement in operating performance

In the IFBC Sector Report – Swiss Retailbanking, we once again present our latest assessments of the financial performance and value creation of Swiss retail banks. In addition, we analyze the stock prices and valuations of listed Swiss retail banks. The published annual financial statements of 55 retail banks provide a comprehensive data foundation. We hope you find these insights valuable and look forward to engaging in dialogue with you as your partner.

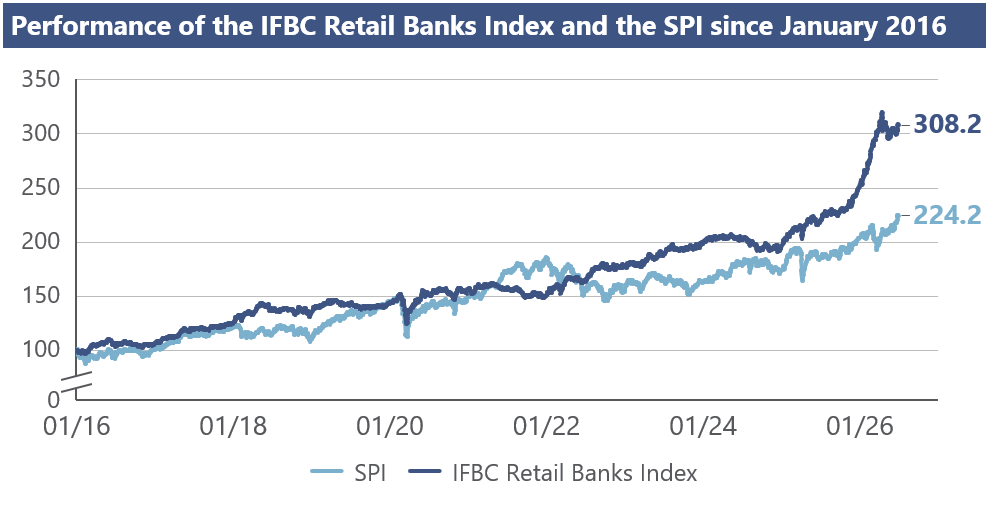

The IFBC Retail Banks Index, which comprises all 15 listed Swiss retail banks, rose by 29.3% in 2025. This increase was significantly higher than the SPI’s performance in 2025 (+17.8%).

Following an exceptionally successful year in 2023, Swiss retail banks’ net interest income declined on average for the second consecutive year (-0.3 pp to -3.1%).

Following a decline of 0.4 percentage points in 2024, the average return on equity of Swiss retail banks fell by a further 0.7 percentage points to 5.1% in 2025.

Christian Hirzel, Partner, Financial Services: “Especially in a challenging market environment, overall bank management based on a solid strategic direction is one of the key success factors.”

The performance of the IFBC Retail Banks Index and the SPI since January 2016

The exceptional increase in the market valuations of Swiss Retail Banks in 2025 was not driven by significant improvements in operating performance. Instead, other factors, such as investors' search for safe-haven assets in an environment marked by heightened uncertainty, were the main drivers of the rise in share prices. Whether these share price increases can be sustained remains uncertain.

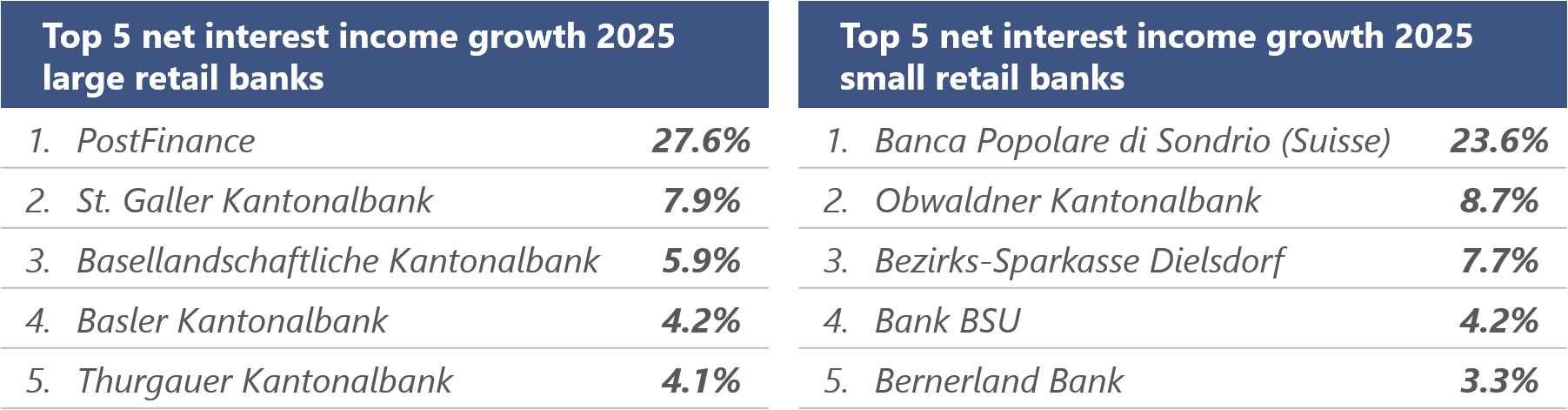

The top 5 for net interest income growth

In a low-interest-rate environment, revenue diversification is key, and expanding non-interest-rate-sensitive business continues to gain strategic importance. A broad revenue base ensures retail banks’ resilience to interest rate changes and sustainably high profitability and return on equity.

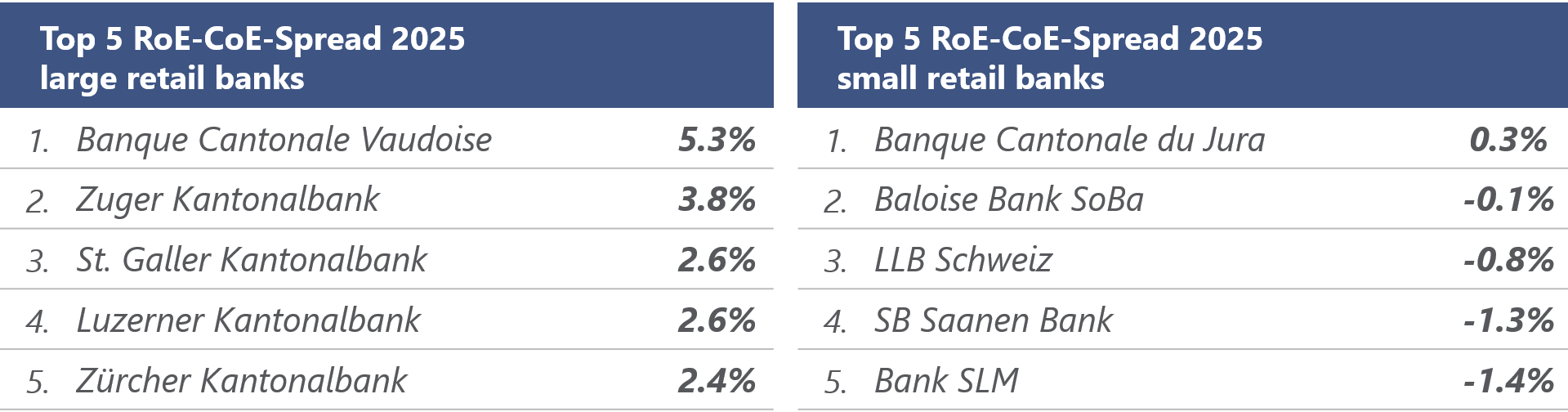

The top 5 for economic profit

The combination of declining interest income and rising operating expenses is weighing on the profitability of Swiss retail banks. Against this backdrop, the average return on equity also came under further pressure. In addition to profitability, return on equity must also be given greater attention and actively managed.

Noel Sager, Director of Financial Services: “Small Swiss retail banks should give greater consideration to strategic options for achieving economies of scale by joining a banking group or carrying out corporate transactions.”

Declining Interest Income

The high dependency on the interest-rate-based business continues to pose a key strategic challenge for Swiss retail banks. To overcome this issue and ensure sustainable economic value creation, there exist various success factors (dynamic planning of interest-rate scenarios, implementation of transparent and sustainable credit pricing, ensuring a high level of professionalism and maturity in treasury, etc.).

Consolidation

For small retail banks in particular, achieving sufficient profitability from a sustainable perspective is becoming an increasing challenge due to the current interest rate environment and rising cost pressures (tighter regulation, digitalization). It must be assumed that consolidation will take place in the Swiss retailbanking market in the coming years.

IFBC Sector Report - Swiss Retailbanking

(The document is available in German only.)

IFBC supports its clients in the banking sector in effectively designing financial management systems, executing corporate transactions, and performing valuations. For detailed insights from the study, please contact: Christian Hirzel and Noel Sager.

More information about Financial Services.

Also of interest to you, our article on best practice in financial bank management at Swiss banks.