.svg)

Swiss software companies are convincing – strategic buyers increase acquisition activity in the software space and remain active in IT services

Download: Technology Report – M&A Insights 2025 (in German)

Rapid technological change, regulatory pressure, and global competition are transforming the Swiss market for software and IT services. Medium-sized providers in particular must make the right strategic decisions to remain competitive and transactional in an environment characterized by megatrends such as cloud platforms, artificial intelligence, and increasing demands for digital trustworthiness.

The IFBC Technology Report presents the current investor view of the sector and highlights strategic implications for companies from a transaction perspective. Furthermore, the report evaluates and comments on all 147 Swiss IT deals in 2025 and analyzes the importance of growth and profitability for the valuation of companies in the industry.

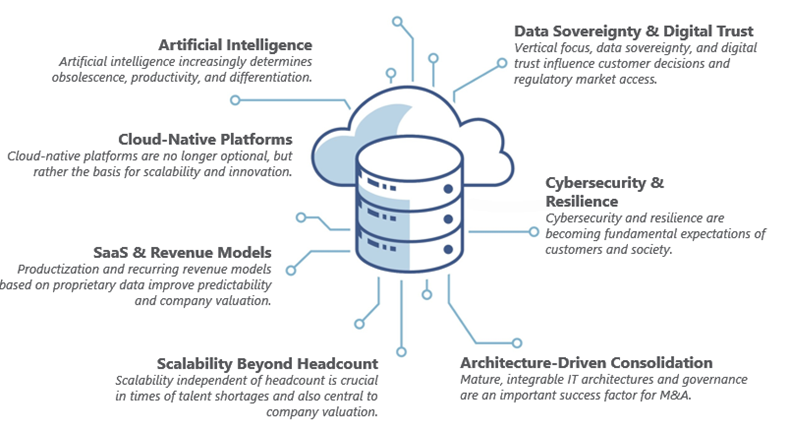

The following seven megatrends describe key technological and structural developments that are having a lasting impact on markets, business models, and competitive dynamics.

The megatrends described highlight the changes that are strategically relevant for Swiss software and IT services companies, including from a transaction perspective. This results in the following concrete implications for competition and value creation among Swiss software and IT companies.

Software providers are increasingly shifting their focus from function-driven competition to platform-based differentiation. The integration of artificial intelligence into products, cloud-native architectures, and recurring revenue models are shaping the strategic positioning of many software companies. Providers with modular product structures, scalable business models, robust governance, and low dependencies are structurally better positioned for high margins and sustainable growth and are therefore more attractive acquisition targets.

IT service providers are under increasing pressure to move away from growth models based on staff expansion. Automation, vertical specialization, AI-supported service delivery, and managed service models are becoming key success factors from a transaction perspective. At the sametime, data sovereignty and the growing importance of trust (security,reliability, and compliance) are defining new requirements. The latterparticularly favors locally anchored providers focused on verticals (sectors)with proven and trustworthy operating models.

Fabian Forrer, CFA, Partner and Sector Lead Technology at IFBC: “Strategic M&A readiness – tailored to the specific challenges of the sector – will be crucial for successful transactions in 2026.”

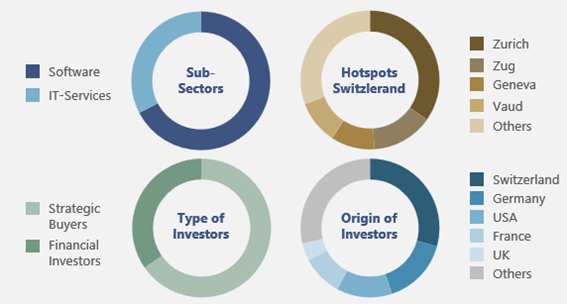

The Swiss IT sector is strongly influenced by strategic buyers when it comes to M&A transactions. In addition, there are currently significantly more transactions in the software sector than in the IT services sector. Zurich is the most important Swiss hotspot, followed by the canton of Zug and the western Swiss hotspots of Geneva and Vaud.

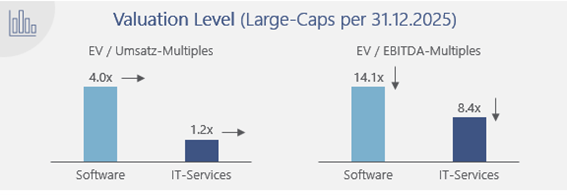

Software companies continue to be valued at higher multiples than companies in the IT services field. In both sub-sectors, EV/EBITDA multiples have declined compared to the previous year.

The detailed analysis in the IFBC Technology Report shows that profitability currently beats “pure” growth for established companies; at the same time, size remains a relevant value driver, even if small/mid-caps can partially relativize the size premium through standardization, pricing power, and revenue visibility. Sector-specific analyses, analyst expectations, and further insights can be found in the complete IFBC Technology Report 2025.

Conclusion

The Swiss software and IT services market is undergoing change. In this environment, buyers are paying particular attention to the quality of IT architecture, the targeted integration of artificial intelligence, scalability, governance, and revenue quality. Companies that align their business models with the Megatrends in Technology that are relevant to them are better positioned to remain competitive in the long term, thereby strengthening their attractiveness for strategic partnerships and M&A activities.

Download: Technology Report – M&A Insights 2025 (in German)

More information on Mergers & Acquisitions.