.svg)

High buying and selling pressure characterizes the Swiss Private Equity market – lower interest rates and more stable valuation expectations create recovery trends for 2026

.png)

Two forces are currently at play in the Swiss PE market: selling pressure on long-held portfolios with insufficient capital returns to investors, and buying pressure due to a high level of dry powder. The result is not yet a broad upturn in the short term, but rather opportunistic transactions in which transaction structure and process quality are important. However, the third quarter of 2025 shows initial signs of recovery and could thus usher in the hoped-for broad upturn in 2026.

Key takeaways

The number of PE deals has remained relatively stable since 2021. Deal volume, on the other hand, fluctuates significantly, as individual periods are characterized by isolated large transactions. Deal volume currently remains below the 2021 level.

This illustrates that even though PE funds have considerable dry powder at their disposal, differing valuation expectations between buyers and sellers, the interest rate environment, and geopolitical and economic uncertainties can slow down transaction momentum. This leads to slower acquisitions, more difficult exit conditions, and, as a result, longer holding periods, which is particularly evident in the case of larger investments. At the same time, small to medium-sized transactions with local champions and SMEs with untapped potential offer PE investors the opportunity to achieve attractive returns with comparatively low leverage.

After deal volume was even more moderate in the second quarter of 2025 due to uncertainties surrounding the US tariff debate, the first signs of recovery are emerging in the third quarter of 2025.

Overview of PE deal activity in Switzerland

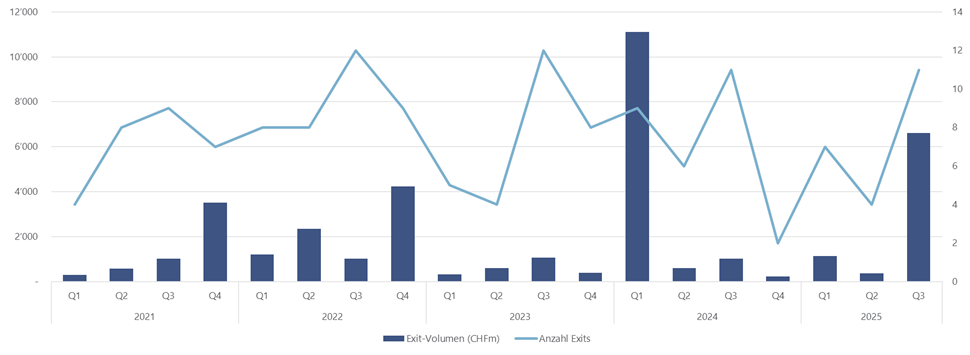

The number of exits in the Swiss PE market has declined since 2022. The exit volume fluctuates more strongly due to size differences in transactions, with a few large exits in individual quarters. For example, the high exit volume in Q1 2024 is almost entirely attributable to the IPO of Galderma.

The increased transaction duration and the postponement of transactions are leading to longer holding periods and a slower return of capital to limited partners, combined with corresponding pressure on returns.

However, the first signs of recovery are also evident in exit activities in the third quarter of 2025.

Overview of PE exit activities in Switzerland

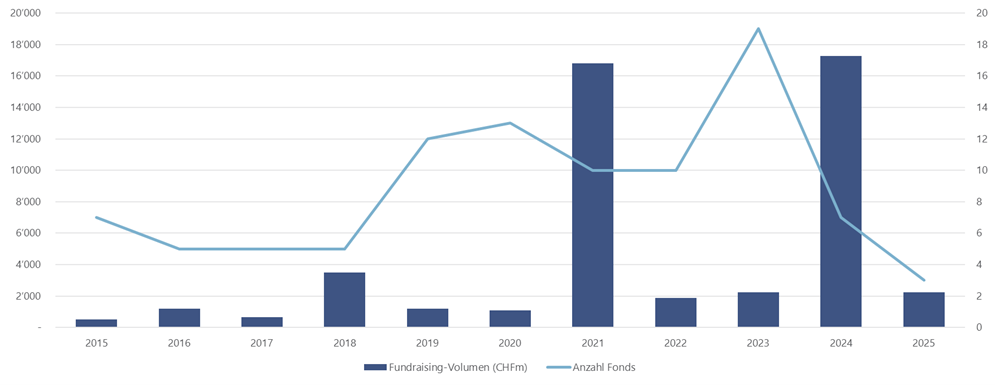

There has been a significant decline in both the volume and number of new funds raised by PE companies in Switzerland. At the same time, fundraising processes are taking longer. A key reason for this is the delayed response of limited partners, who typically only increase their capital commitments once returns from exits have been realized. As exit activity has fallen short of expectations in recent years, fundraising has slowed accordingly. In addition, the dry powder from previous fundraising rounds is increasing the investment pressure on PEs.

In smaller markets such as Switzerland, with a manageable number of active PE investors, fundraising is naturally very cyclical. It is therefore not possible to draw any immediate conclusions about deal activity from fundraising activity.

Overview of fundraising activities by PEs in Switzerland

Conclusion

The Swiss PE market remains transactional but opportunistic, with a focus on local champions and SMEs with untapped potential that are less susceptible to (global) macroeconomic headwinds. Selling pressure on more mature portfolio companies is counterbalanced by buying pressure from existing dry powder. Transactions are primarily realized when the transaction structure and process quality can bridge any valuation differences, or when attractive entry prices are available. Fundraising by PE companies in Switzerland follows this development with a time lag and cyclical fluctuations.

The third quarter of 2025 shows initial signs of recovery: lower interest rates and increasing buying and selling pressure from PE investors are likely to lead to a convergence of valuation expectations between buyers and sellers and support a broad upturn in transaction activity in 2026.

Thanks to our in-depth knowledge of the Swiss PE landscape and the investor environment, we support our clients in implementing transactions successfully, both strategically and operationally.

More information about IFBC Services.

M&A | Due Diligence | Value-based Management | Valuation & Financial Modeling | Debt Advisory