.svg)

Consolidation, innovation and disciplined dealmaking are driving M&A activity amid a complex geopolitical environment

Download: Healthcare & Lifesciences Report 2026

The global M&A market has recently recovered significantly, including in the Healthcare & Lifesciences sector. At the same time, geopolitical tensions and macroeconomic uncertainties persist, particularly in connection with tariffs and supply chain risks. Nevertheless, IFBC expects transaction activity to rise in 2026. At the same time, the continued high level of investment selectivity is leading to ongoing caution in the M&A market. The focus is on high-quality assets and strategically aligned business models.

The IFBC Healthcare & Lifesciences Report analyzes M&A activity in 2025 and provides an outlook for 2026 – with a particular focus on the European and Swiss markets.

The biopharma subsector is facing a structural turning point: Over USD 600 billion in revenue will lose patent protection over the next ten years – oncology and immunology are particularly affected. For companies like Novartis, which will lose around 20% of their revenue base solely due to expiring patents, M&A is no longer an option but a strategic necessity.

At the same time, China is reshaping the global innovation landscape: Chinese biotech firms are rapidly and cost-effectively developing new active ingredients—from ADCs (antibody-drug conjugates) to GLP-1 receptor agonists. Western pharmaceutical companies are increasingly licensing these assets, thereby securing access to innovation without having to shoulder the entire development process and its costs themselves. By 2025, Chinese companies accounted for 30% to 40% of global pharmaceutical licensing activity – a trend that will continue to grow in 2026.

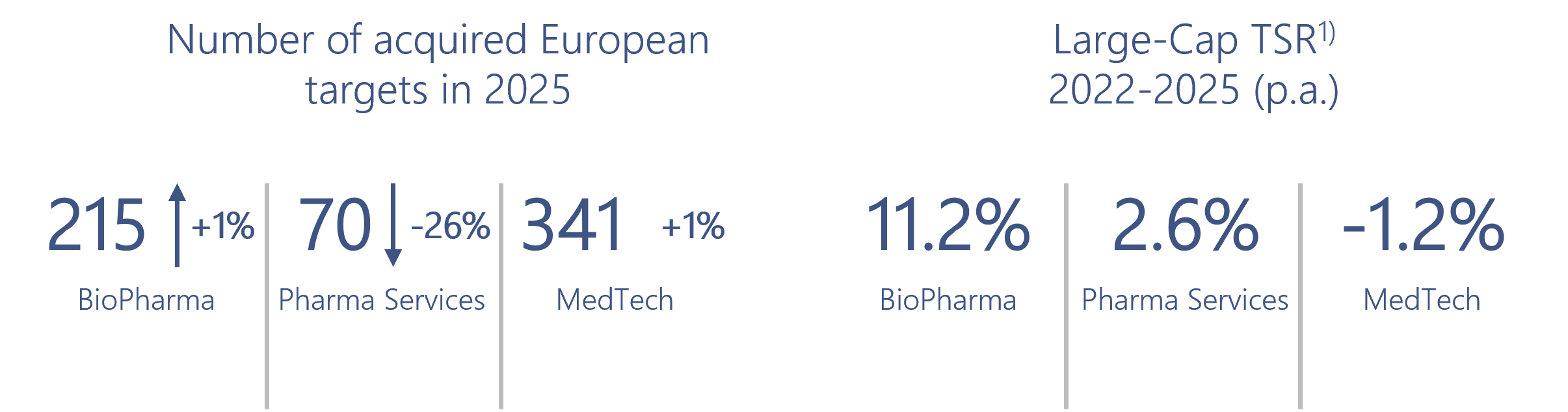

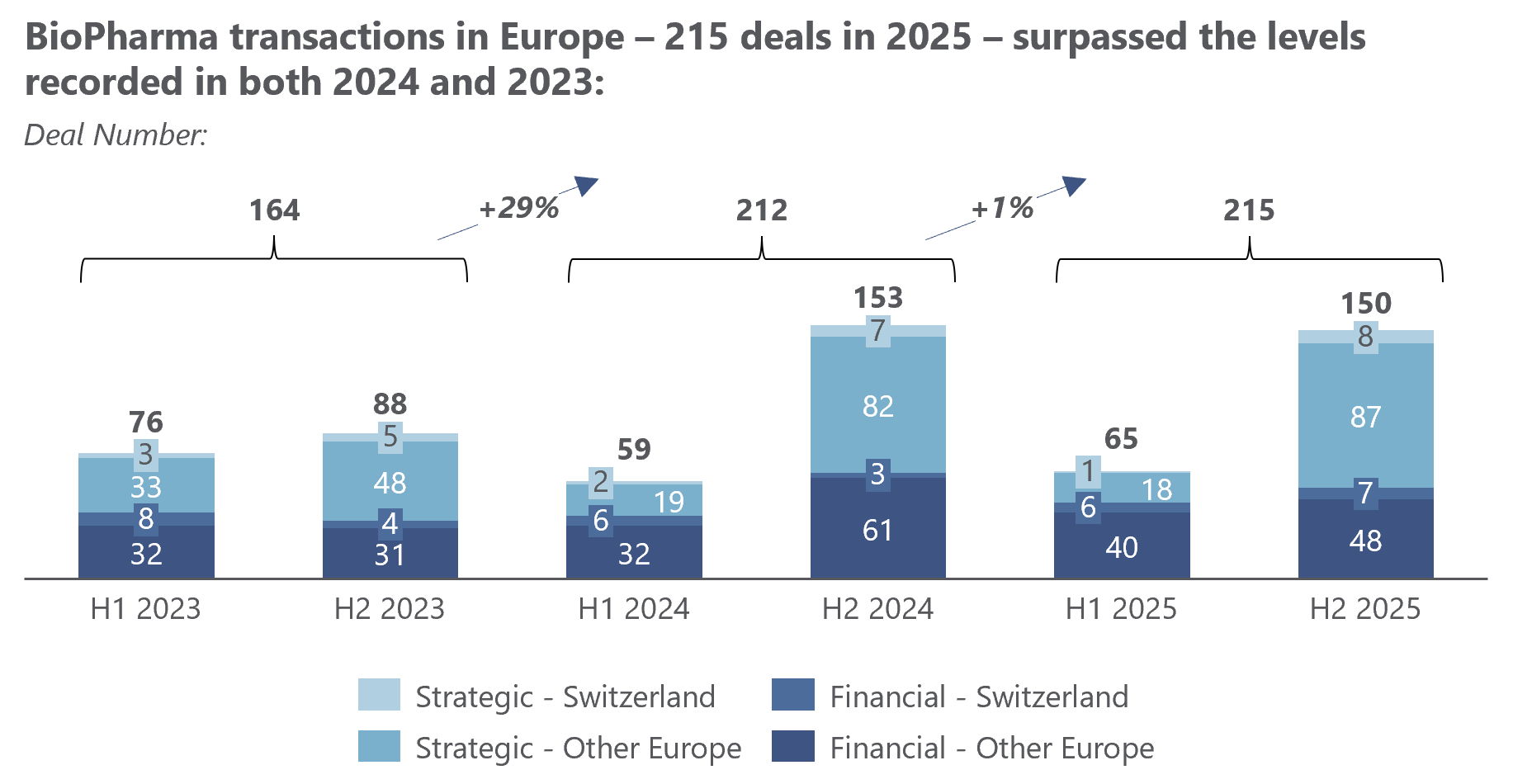

Biopharma transactions in Europe rose to 215 deals in 2025, with a significant increase in deals exceeding EUR 1 billion.

In the pharmaceutical services sector – namely CDMOs (contract development and manufacturing organizations) and CROs (contract research organizations) and CDMOs – the focus of M&A has shifted fundamentally: Instead of merely gaining size through acquisitions (“scale”), the priority today is securing specialized production capacities and technological expertise (“scope”). Providers are making targeted investments in the production of complex active ingredients, using AI to accelerate drug development, and diversifying their geographic presence to reduce supply chain risks.

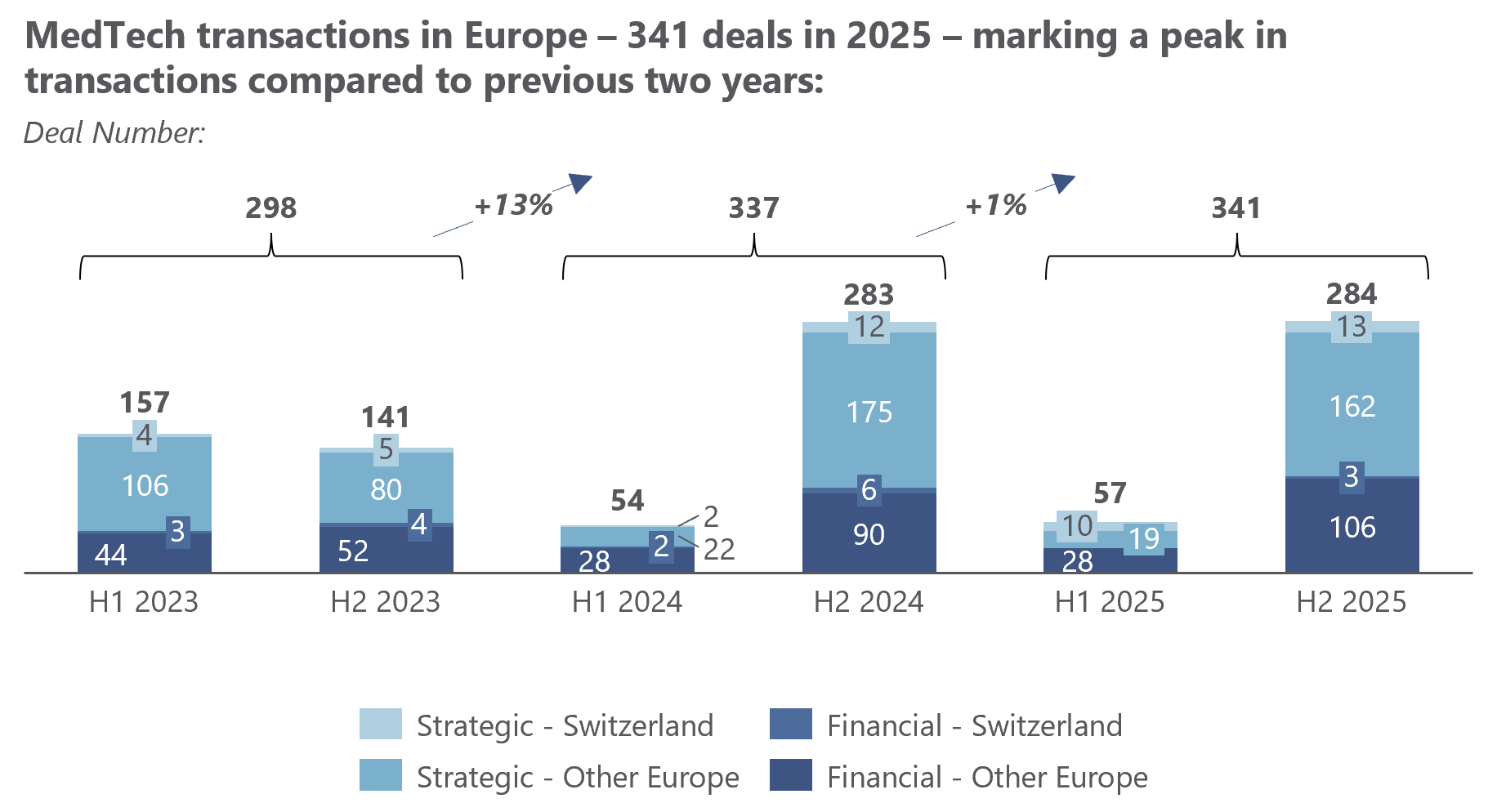

Particularly in demand: capacity for peptides, BsAbs (bispecific antibodies), and ADCs (antibody-drug conjugates), driven by new innovative drugs, especially in the fields of oncology, immunology, and obesity. The global peptide CDMO market is predicted to grow to approximately USD 11 billion by 2032. While deal activity in Europe fell to 70 transactions in 2025 (–26%), high-value deals – often driven by private equity investors – remained steady.

The Swiss MedTech subsector is heavily dominated by SMEs – and it is precisely these companies that are currently under considerable pressure: Geopolitical trade tensions, tariff uncertainties, and growing local price pressure are weighing on business, particularly since the U.S. is one of the most important export markets. Large companies like Straumann are responding by establishing their own U.S. production facilities – though this is often not a realistic option for many SMEs.

At the same time, AI integration, robotics, and patient-centered care models are opening up new growth opportunities. The number of M&A transactions in Europe reached a new high of 341 deals in 2025 – a sign that consolidation pressure, as well as strategic opportunities, continue to grow.

“Companies that act decisively now – through partnerships, acquisitions, or the divestiture of non-strategic business units – will secure the best starting positions in an increasingly selective market,” says Michel Le Bars, Partner and Sector Lead for Healthcare & Lifesciencesat IFBC.

The Swiss Healthcare & Lifesciences market is undergoing a transformation. In all three subsectors – Biopharma, Pharma Services, and MedTech – consolidation pressure and strategic demands are rising. Companies that proactively align their business models, whether through targeted acquisitions, partnerships, or the divestiture of non-strategic assets, strengthen their competitiveness and their attractiveness for strategic transactions.

Download: Healthcare & Lifesciences Report 2026

More information on Healthcare & Lifesciences