.svg)

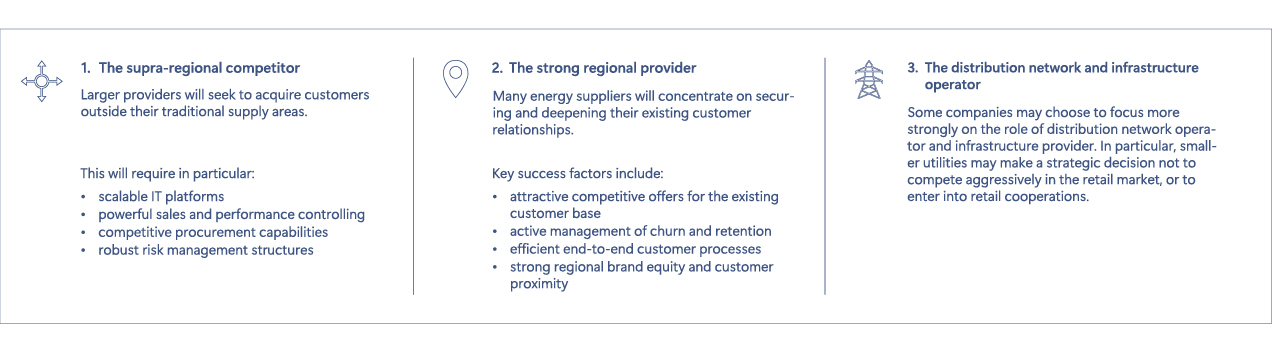

Why customer loyalty is becoming a key competitive factor in the liberalized electricity market.

The planned full liberalization of the Swiss electricity market is once again being intensively debated in light of a potential electricity agreement between Switzerland and the EU. The discussion frequently centers on the expectation of intense competition for residential customers. However, experience from other liberalized electricity markets points to a different pattern: going forward, the economic success of an energy supplier will depend less on acquiring new customers and far more on its ability to delight and retain its existing customer base over the long term.

Even after a potential market opening, regulated universal service (basic supply) will remain in place in Switzerland. Households and smaller businesses with annual consumption below 50 MWh will retain the right to remain in, or return to, the basic supply regime. This gives rise to a market model already familiar from other European countries: an open competitive market combined with a structurally strong position for the incumbent regional suppliers. In such a market scenario, many energy suppliers face a central strategic question: how can they economically defend their existing customer base when it becomes much easier for customers to switch providers?

A look at other European power markets shows that established energy suppliers have, contrary to many forecasts, largely been able to defend their market position over the long term. In Germany, for example, the electricity market has been fully liberalized for more than twenty years. Nevertheless, in 2023 around 24% of residential electricity volumes were still supplied under basic supply tariffs. A further ~38% related to competitive contracts concluded with the local basic supplier. Taken together, the local incumbent suppliers continued to serve around 60% of the residential market in that year. Many customers remained loyal to their existing provider, even though they would have been able to switch. The reasons most frequently cited are customer inertia as well as the quality of service provided by the incumbent suppliers.

These insights are central for Swiss energy suppliers as they prepare for full market opening. While liberalization does lead to competition, it does not automatically trigger a large-scale displacement of local suppliers. Competition is likely to take place primarily between established regional suppliers, a limited number of supra-regional providers and specialised market participants.

Christian Hirzel, Partner at IFBC: „The planned full market opening will, for Swiss energy suppliers, be less a race for growth and more a race for profitable customer retention and operational efficiency.“

A second pattern observed in liberalized energy markets is the concentration of market share in the competitive retail segment. The UK provides an illustrative example: at the end of 2024, the six largest providers accounted for around 91% of the market for domestic customers. Many smaller challengers, often highly specialized in energy retail, were forced out of the market during the energy crisis from 2021 onwards. These insolvencies were driven in particular by inadequate hedging strategies, insufficient liquidity reserves and a weak equity base. Furthermore, the regulator-defined price cap prevented a full pass-through of significantly higher procurement costs to end customers.

The reasons for the market concentration observed in many countries’ energy retail segments lie largely in the economic structure of the business.

Energy retail in particular requires:

These structures generate high fixed costs. Providers with a large customer base can allocate these costs far more efficiently. For smaller energy suppliers, it will therefore be challenging to achieve significant growth outside their traditional supply areas. As a result, many suppliers will need to focus on developing strategies and optimising structures and processes aimed at retaining their existing customer base over the long term.

Growing pressure to achieve scale is also likely to foster new cooperation and consolidation models over the medium term. Potential options include joint retail platforms, cooperations in billing or energy procurement, as well as mergers and acquisitions between suppliers.

Historically, the retail business has not been a strategic steering field for many Swiss energy suppliers. Sales volumes were relatively stable, customer churn was minimal, and pricing structures were largely regulated. Market opening will change this logic. Going forward, the profitability of the residential segment will be far more strongly driven by commercial and sales management levers.

Key metrics will include in particular:

This will fundamentally change the way the retail business is managed financially. Whereas the focus to date has primarily been on sales volumes and energy procurement, going forward customer value, customer retention and sales productivity will be at the forefront. The central business question therefore becomes: how much economic value does a company lose when a customer switches – and how much is it rational to invest in retaining that customer?

Full market opening will affect not only the retail function but also energy management. As residential and small business customers will in future be able to switch more easily between competitive market offers and basic supply, the sales base will become more volatile. This complicates forecasting for procurement and hedging.

Companies will therefore need to integrate their processes more closely across:

The energy crisis in the UK in 2021 and 2022 demonstrated how risky growth strategies in electricity retail can be if they are not supported by robust procurement and risk management structures. Numerous providers were forced to exit the market. For Swiss energy suppliers, it will thus be critical to tightly interlink retail and risk management. At the same time, as outlined above, operational efficiency will become a key competitive factor.

Against this backdrop, three likely strategic role models are emerging for many energy suppliers.

The planned full market opening will, for Swiss energy providers, be less a race for growth than a contest for profitable customer retention and operational efficiency.

The ability of suppliers to succeed in a competitive market will depend primarily on how effectively they can build the following capabilities:

Energy suppliers that master these capabilities will be well positioned to defend and strengthen their market position even in a fully liberalized electricity market.

For small and mid-sized energy supppliers, this will increasingly raise a fundamental strategic question: can the required scale in competitive retail be achieved independently – or will the strategic focus in the long run be more on grid operations, infrastructure, and partnerships?

More information about Energy