.svg)

M&A activity is likely to remain high in 2026

The global M&A market recovered significantly in 2025, and the same applies to the Swiss market. Despite ongoing geopolitical tensions and economic uncertainties, 2025 was a very active transaction year in a multi-year comparison, both in terms of deal value and number of transactions. This shows that market participants have increasingly adapted to challenging conditions. We expect the transaction environment to remain active in 2026, supported by attractive macroeconomic conditions and strategic drivers.

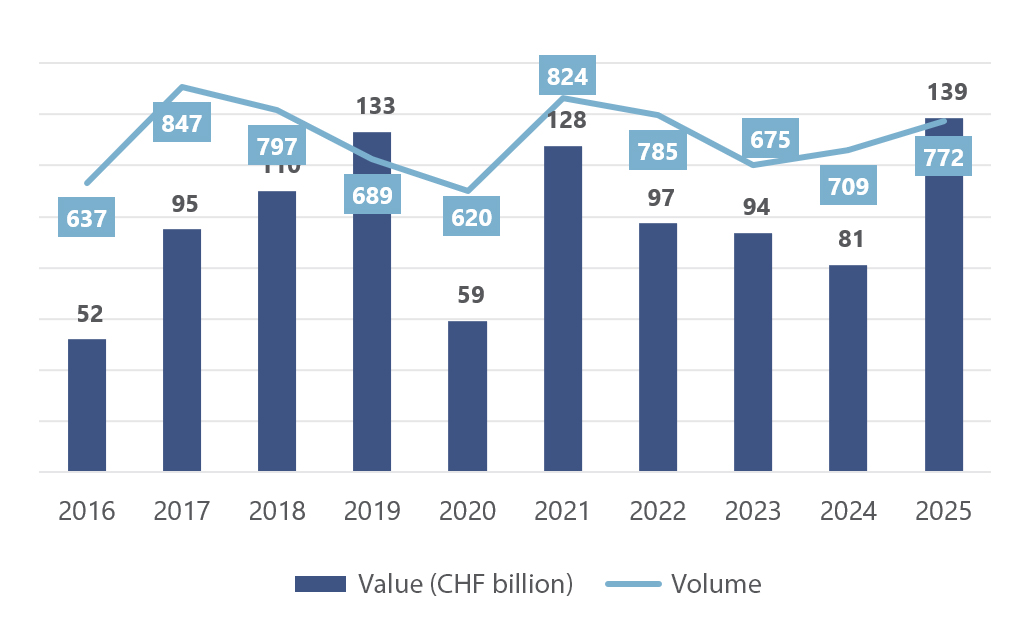

Despite geopolitical tensions and economic uncertainties, the deal value in 2025 reached a level last seen in 2021. The increase is mainly attributable to several mega-transactions. In the Swiss market, four transactions with a value of more than CHF 10.0 billion each were recorded in 2025. This is a figure that has not been exceeded in the past ten years. These mega-transactions include the spin-off and sale of Amrize by Holcim with a transaction value of around CHF 27.5 billion, the largest M&A transaction in Switzerland in 2025. In addition, there were just under 50 transactions with a value of over CHF 0.5 billion (large transactions). Here, too, the level was only slightly exceeded in 2021 over the past ten years. The driving forces behind this were both the fall in interest rates in Switzerland, which made it easier to finance large transactions, and clear strategic considerations on the part of investors:

In addition, there was a high level of activity among PE investors, particularly in the second half of the year. For example, Ufenau Capital Partners completed 52 transactions in Switzerland and abroad as part of its buy-and-build strategy. The increase in PE activity is attributable both to growing pressure to sell longer-held portfolios and to sustained investment pressure as a result of high dry powder reserves. This momentum, supported by lower interest rates in 2025, also favored larger PE transactions, such as the acquisition of Techem by Partners Group (CHF 6.2 billion).

The number of transactions rose less sharply than the deal value. In 2025, Swiss companies were involved in a total of 772 deals as buyers, sellers, or target companies, with an aggregate disclosed transaction value of over CHF 139 billion. With 158 transactions, the technology sector led the way in terms of number of transactions, continuing the trend of recent years. The drivers for this are technological advances, particularly in the areas of AI, cyber resilience, and cloud modernization (see 7 Megatrends of the IFBC Technology Report). The healthcare sector, on the other hand, recorded the highest transaction value, which is not surprising given the importance of Swiss market leaders Roche and Novartis. Major deals included the acquisitions of Avidity Biosciences (CHF 10.1 billion) and Argo Biopharma (CHF 4.3 billion) by Novartis, and Zealand Pharma (CHF 4.6 billion) and 89Bio (CHF 2.9 billion) by Roche.

The strong Swiss franc proved to be a clear strategic advantage for Swiss buyers in 2025, increasing their purchasing power, especially for cross-border acquisitions. Swiss companies carried out a total of 316 transactions abroad. At the same time, Switzerland's high economic and political stability increased the attractiveness of Swiss target companies for international investors: foreign buyers acquired 213 companies in Switzerland, a significant increase compared to previous years. In comparison, transaction activity within Switzerland remained moderate at 127 deals, even when compared to previous years.

In 2025, nearly CHF 3.0 billion in venture capital was also invested in Swiss start-ups, with Windward Bio, Climeworks, Distalmotion, GlycoEra, and Auterion receiving more than CHF 600 million combined.

In 2025, IFBC advised on a total of 11 transactions in the focus sectors of energy, industrials, healthcare & life sciences, technology, and financial services. Of these, 10 were mandates with a Swiss target company, with an aggregate transaction value of around CHF 15.6 billion. These included several of the most significant public M&A transactions in Switzerland, namely the mergers of Baloise and Helvetia as well as Ina Invest and Cham Group, the spin-off of Ypsomed Diabetes Care AG, and the acquisition of Global Blue by Shift4 and u-blox by Advent.

In addition, our M&A team supported energy pioneer naturenergie in its acquisition of Swiss solar company Solan and RS Properties in its majority takeover of the wellness area of the Parkresort Rheinfelden from Invision. IFBC also acted as exclusive financial advisor to founder and owner Prof. Dr. Janssen on two sales: the successful sale of Finfox to the Chapters Group and Ecofin Investment Consulting to Vaudoise Insurance. Finally, IFBC and its Globalscope partner advised Burckhardt Compression on its acquisition of US service company ACT (Advanced Compressor Technology).

Source: Mergermarket, criterion: transactions with a Swiss target company and majority stake.

Transaction activity in the Swiss M&A market is expected to remain high in 2026. In addition to the strong Swiss franc and the attractiveness of Swiss target companies, the drivers are likely to be the decline in financing costs in Switzerland since 2025 and a solid valuation level. Nevertheless, certain global economic and geopolitical uncertainties remain.

In addition to expected mega-transactions by Swiss market leaders (e.g., Nestlé Water) and upcoming succession arrangements at SMEs, M&A activity in 2026 is likely to be influenced primarily by the following factors:

PE investors remain key market participants. With record reserves ("dry powder"), considerable capital remains available for targeted investments in attractive companies. At the same time, there is increasing pressure to actively manage existing portfolios, which favors both add-on acquisitions and divestitures.

However, the improved conditions and sector-specific trends will not lead to a broad-based M&A boom. Although market participants are becoming increasingly accustomed to uncertainty, investment discipline has increased in recent years. Transactions are not carried out solely on the basis of available liquidity and financing, but selectively and out of conviction. The focus remains on solid business models with sustainable cash flows and a clear equity strategy. In addition to the quality of the target companies, a well-prepared, professionally managed M&A process and realistic valuation expectations remain crucial for the success of a transaction. M&A transactions in saturated markets with little growth potential and low margins could become correspondingly more challenging. In these cases, transaction prices will come under further pressure and the requirements for transaction structuring will increase.

In 2025, the Swiss M&A market demonstrated that transactions can be successfully implemented even in a challenging environment. Lower financing costs facilitated large transactions in particular, while companies took advantage of attractive growth, consolidation, and divestment opportunities. Activity is expected to remain high in 2026, supported by persistently low financing costs, technological developments (especially in the field of AI), and an increase in scale and scope deals, as well as buying and selling pressure on private equity investors. The strong Swiss franc boosts purchasing power in cross-border transactions, while the high attractiveness of the location ensures international interest on the seller side. However, we expect investment discipline to remain high, with the focus on solid business models with sustainable cash flows. In saturated markets with limited growth and margin potential, transaction prices could come under pressure, making the structuring of complex deals more important.